Home improvement loans London: the complete 2026 guide

Home improvement loans in London in 2026: compare secured and unsecured borrowing, APRs, loan limits, total cost, eligibility and how to fund an extension or renovation.

How to use this guide

- Read with your project scope and budget envelope in mind.

- Use it to brief designers and compare quotations more rigorously.

- Raise any project-specific constraints with us before committing to a contractor.

Home Improvement Loans London: The 2026 Guide

A home improvement loan in London is usually an unsecured personal loan of £1,000---£25,000 (some lenders reach £35,000---£50,000) at a representative 5.9---9% APR in mid-2026. Above roughly £25,000 - where most London loft conversions and extensions sit - a secured loan or remortgage at 6.39---12% almost always works out cheaper. Match the product to the real project cost, not the headline rate.

Key takeaways

Unsecured personal loans cap out fast. Most mainstream lenders stop at £25,000, a few reach £35,000---£50,000. That ceiling is the single most important number for a London homeowner, because a rear dormer here starts around £45,000.

Secured beats unsecured on cost above £25k. In June 2026, secured (second-charge) rates ran from 6.39% for clean credit at low loan-to-value up to about 12% - and let you borrow the £50,000---£130,000 a real London project needs.

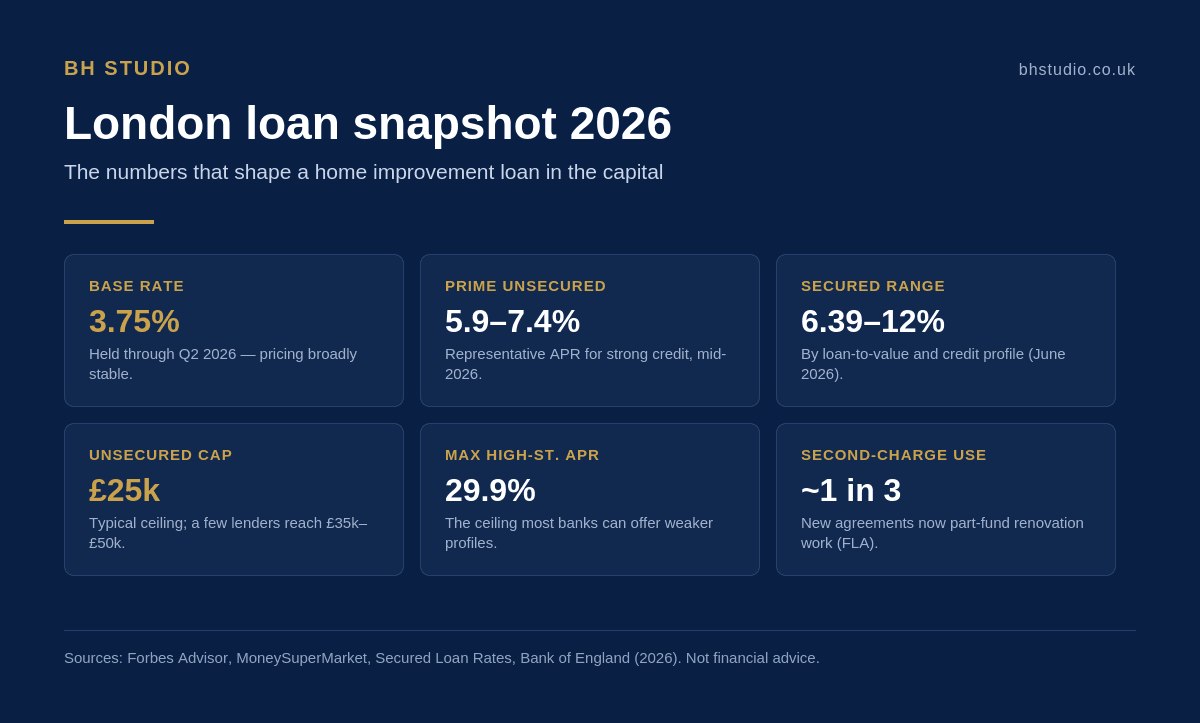

The Bank of England base rate is 3.75%. Held through Q2 2026, so pricing has been broadly stable. Prime unsecured deals sit at 5.9---7.4% representative; your actual rate depends on credit profile and amount.

A loan is not the only route. Remortgaging or a further advance is often cheaper still - we cover the full picture in our guide to financing a London extension or renovation. This article focuses specifically on loans.

APR is the number that matters, not the monthly figure. It bundles interest and standard fees into one comparable percentage. A low monthly payment stretched over seven years can quietly cost more than a higher payment over three.

A fixed-price contract strengthens your application. One itemised budget from a single accountable contractor is exactly the financial clarity a lender wants to see.

Budget a 10---15% contingency into what you borrow. London projects hit party-wall costs, scaffold licences and structural surprises. Under-borrowing forces a second, more expensive top-up mid-build.

What this guide covers

What a home improvement loan actually is

A home improvement loan is money borrowed specifically to pay for renovation work, repaid in fixed monthly instalments over a set term. Home improvement loans in London come in two forms: unsecured (no collateral, faster, capped lower) or secured against your home (larger sums, lower rates, more paperwork). The money itself is unremarkable - the choice between the two types is where homeowners win or lose thousands.

Strip away the marketing and there are only two products here. An unsecured personal loan advances you a lump sum you repay over one to seven years, with nothing pledged against it. A secured loan - often a second-charge mortgage - uses your property as collateral, which lets you borrow more, usually at a lower rate, but puts your home at risk if you default. Everything else you will read about "home improvement finance" is a variation on one of those two, or a mortgage-based route we cover elsewhere.

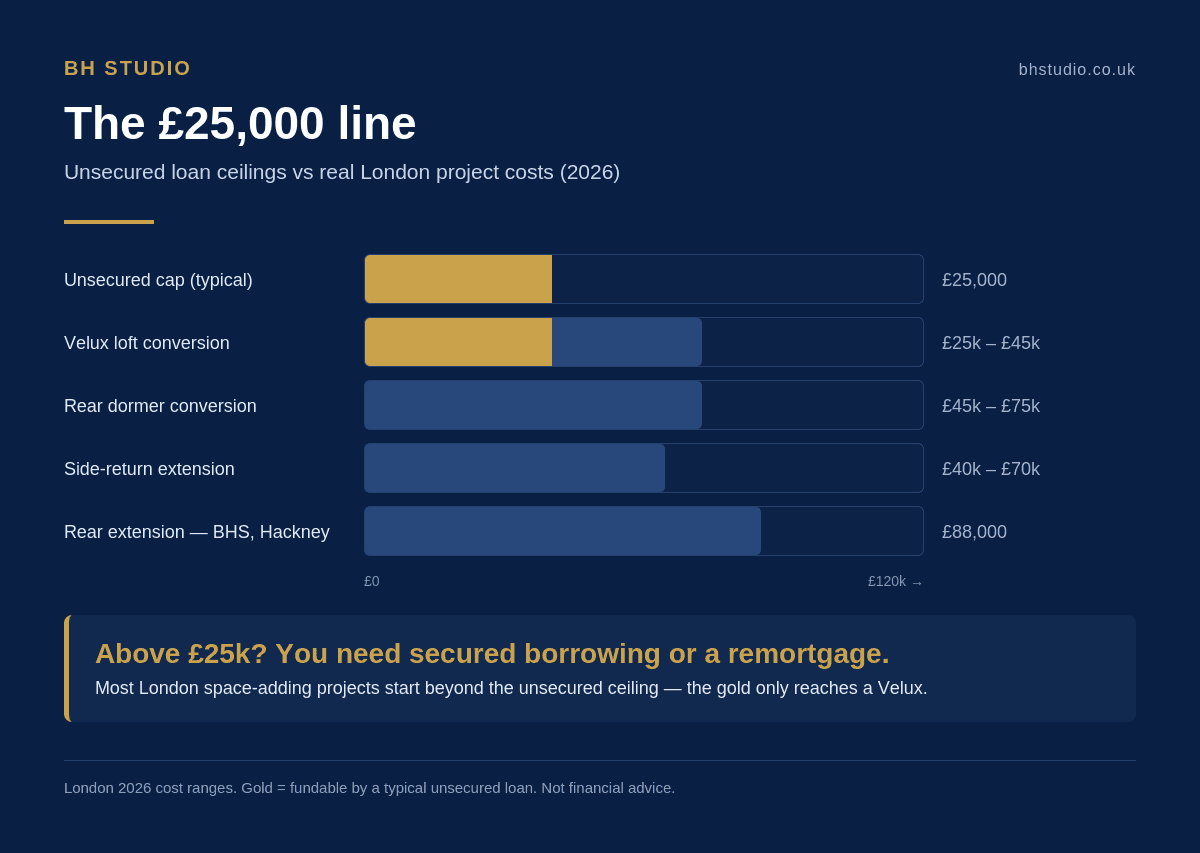

What makes home improvement loans in London a different question from the national market is scale. A guide written for the UK as a whole cheerfully suggests a personal loan for "a new kitchen or a loft conversion." That advice quietly breaks down here, because the cost of the work in the capital routinely exceeds what an unsecured loan will lend. A Velux loft conversion in London runs £25,000---£45,000; a rear dormer, £45,000---£75,000; a side-return extension, £40,000---£70,000. The moment your project crosses £25,000, the neat "just take a personal loan" answer stops applying - and most real London jobs start above that line.

So the useful question isn't "what is a home improvement loan?" It's "which type fits a project of my size, in my borough, at my credit profile?" That's what the rest of this guide answers, with the real numbers behind the decision.

Secured vs unsecured: the real decision

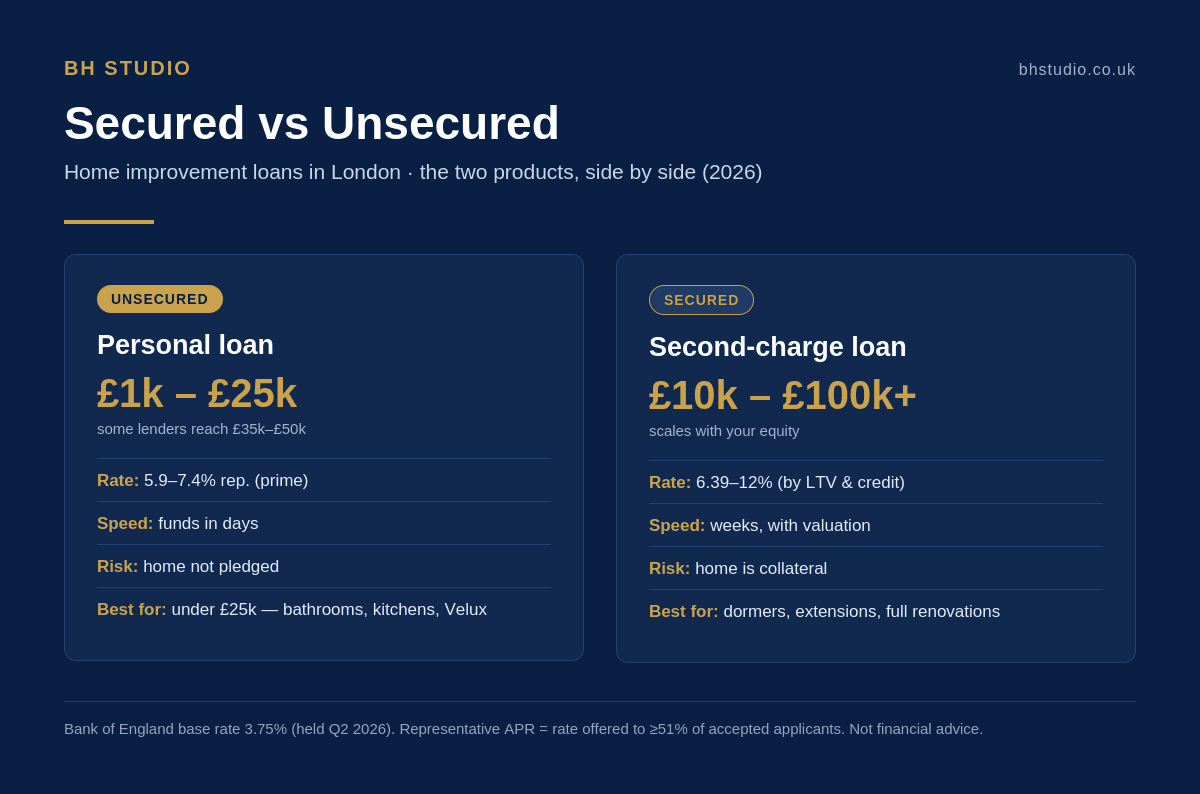

Unsecured loans are faster, put nothing at risk, and suit projects under £25,000. Secured loans let you borrow £10,000 to £100,000+ at lower rates, but your home is on the line and the process takes weeks, not days. For most London renovations, the project cost decides the answer before your preference does.

An unsecured personal loan is the cleaner instrument. There is no valuation, no charge registered against your property, and funds often land within days of approval. If you miss payments, your credit rating suffers badly - but your home is not immediately at risk. The trade-off is a lower borrowing ceiling and a higher rate than any mortgage-backed option.

A secured loan - the lender's term is a second-charge mortgage - sits behind your main mortgage. If the property is ever sold or repossessed, your first lender is repaid before the second. Because the debt is backed by bricks and mortar, rates are lower and the sums much larger: £10,000 to £100,000 and beyond, depending on your equity. This is genuinely mainstream now. Finance & Leasing Association data shows roughly a third of new second-charge agreements in 2026 are used wholly or partly for renovation work - homeowners are increasingly reaching for secured borrowing precisely because unsecured loans can't stretch to a real extension.

Here's the honest framing most comparison sites skip: for a London project, you rarely get to choose based on temperament. If you want a £60,000 side-return extension in Walthamstow, an unsecured loan simply won't lend it. The decision is made by the number on your builder's quote. Which is exactly why an accurate quote - before you approach any lender - matters more than shopping rates. Our full London renovation cost guide and the renovation cost calculator exist to get that number right first.

How much can you actually borrow?

Unsecured personal loans for home improvements typically run £1,000---£25,000, with a handful of lenders reaching £35,000 or £50,000. Secured loans start where those stop and scale into six figures. In London, where a dormer starts near £45,000, that unsecured ceiling is the line most projects cross.

Most mainstream unsecured lenders cap home improvement loans at £25,000. M&S Bank lends £1,000---£30,000; Tesco Bank reaches £35,000; Lloyds and Santander advertise up to £50,000 for the strongest applicants. Above that, you are in secured or remortgage territory. Specialist providers like Novuna push unsecured lending to £35,000, but the representative rate applies to a narrower band (typically £7,500---£25,000), and the amount you're actually offered depends on your income and credit file.

Now lay those ceilings against real London costs. A basic Velux conversion at £25,000---£45,000 sits right on the unsecured boundary - borrowable at the low end, not at the high. A rear dormer at £45,000---£75,000 is beyond every unsecured lender. A single-storey rear extension in Hackney - one of our completed projects came in at £88,000 for 30 square metres - is more than triple the mainstream unsecured cap. The pattern is consistent: unsecured loans comfortably fund a bathroom refit or a kitchen refresh, but the space-adding projects London homeowners most want are secured-loan or remortgage jobs by cost alone.

This is the number to internalise before you do anything else: £25,000. Below it, an unsecured loan is usually the simplest route. Above it, you almost certainly want secured borrowing or to release equity. Everything downstream - rate, term, monthly cost, risk to your home - follows from which side of that line your project lands on.

Rates and APRs in London, 2026

In mid-2026, the best home improvement loans in London carry representative APRs of 5.9---7.4% on the unsecured side for prime borrowers, with maximums up to 29.9%. Secured loans run 6.39% to around 12% depending on credit and loan-to-value. The Bank of England base rate is 3.75%, held through Q2, keeping pricing stable.

Representative APR is the rate a lender must offer at least 51% of accepted applicants - a useful comparison anchor, not a promise. In mid-2026, M&S Bank advertised 5.9% representative on £7,500---£25,000; Tesco Bank 6% for Clubcard holders; Lloyds and Bank of Scotland 7.4% on £7,500---£25,000. Those are the shop windows. The rate you get moves with your credit score, the amount, and the term - and the maximum most high-street lenders can offer is 29.9%.

On the secured side, pricing tracks your loan-to-value and credit quality: roughly 6.39% for clean credit at low LTV, rising toward 12% for adverse credit or higher borrowing against your equity. With the base rate held at 3.75% through the second quarter of 2026, and new entrants sharpening competition at higher loan amounts, secured pricing has been steady rather than volatile - a reasonable environment to borrow into, provided the monthly cost is comfortable even if rates move later.

One trap to name plainly: the headline monthly payment is not the cost of the loan. A seven-year term makes almost any sum look affordable per month while quietly inflating the total interest. Always compare on APR and total amount repayable across the full term - the next section works a real example through end to end.

Loan vs remortgage: which is cheaper?

For projects under £25,000, an unsecured loan's speed and zero property risk often justify its higher rate. For £25,000---£150,000, remortgaging or a further advance almost always costs less per pound borrowed, because secured lending against your home is cheaper than any personal loan. The right answer depends on your existing mortgage as much as the rate.

A personal loan and a remortgage are not really competitors - they serve different project sizes. Under £25,000, a personal loan wins on simplicity: no valuation, no conveyancing, no charge against your home, funds in days. Between £25,000 and £150,000 - the range most London extensions and loft conversions occupy - releasing equity through a remortgage or further advance is materially cheaper, because the debt is secured and spread over your mortgage term.

But cheaper per pound isn't the whole story. If you locked a sub-3% mortgage rate during 2020---2021, breaking it to remortgage could trigger early repayment charges of thousands and lose you that rate on your entire balance. In that situation a further advance or a second-charge loan - keeping the cheap rate on the bulk of your borrowing and paying a higher rate only on the new money - can beat a full remortgage even though the headline secured rate looks worse. This is where a whole-of-market mortgage broker earns their fee: the arithmetic is specific to your existing deal.

We work through remortgaging, further advances, second charges, bridging and staged-release renovation mortgages in full in our London renovation financing guide. If your project is clearly above the £25,000 unsecured ceiling, read that next - this guide covers the loan-shaped slice of a bigger picture.

The total cost of borrowing, worked through

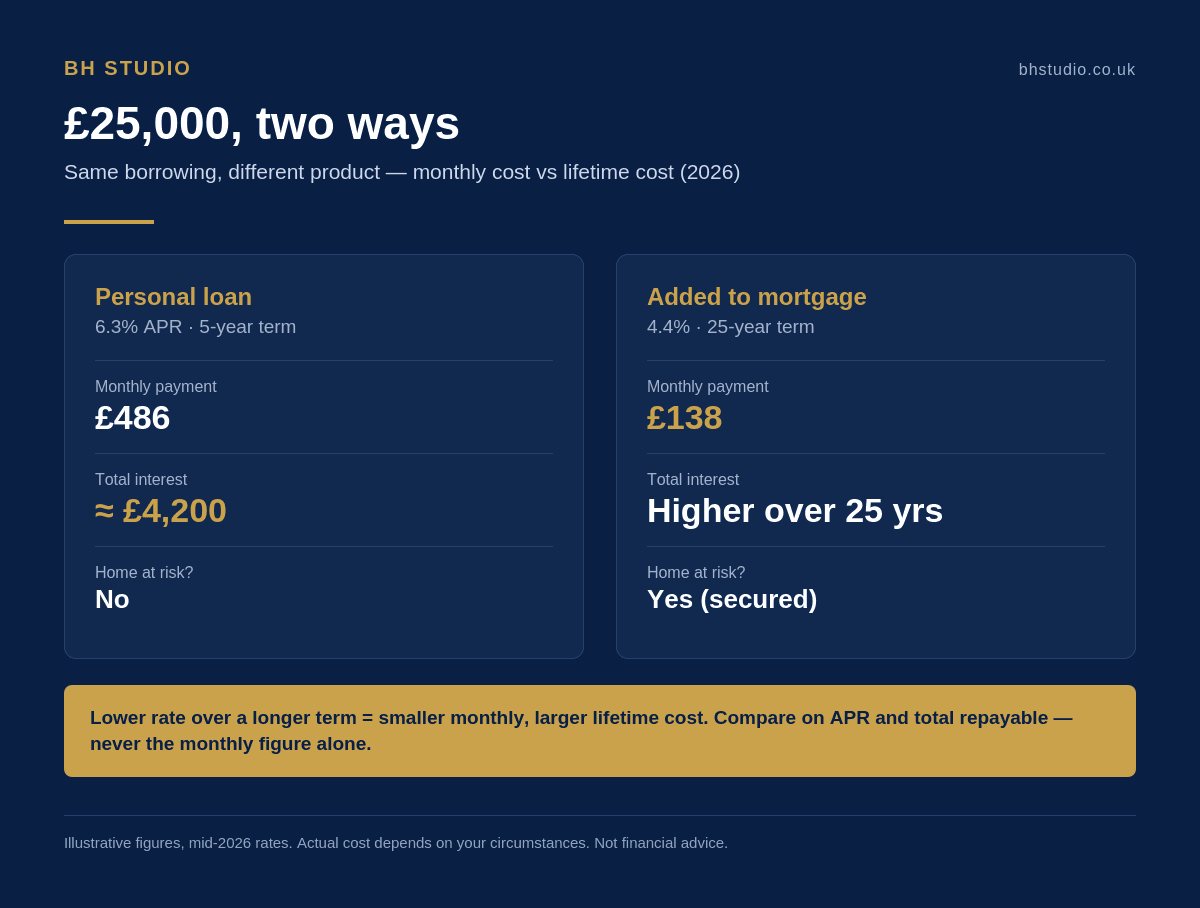

Borrowing £25,000 over five years at 6.3% APR costs roughly £486 a month and about £4,200 in total interest. The same £25,000 added to a mortgage at 4.4% over 25 years costs around £138 a month - but far more interest overall because of the longer term. Lower rate, longer term: smaller monthly, larger lifetime cost.

Numbers make the trade-off concrete. Take a £25,000 kitchen renovation - a project that fits comfortably inside the unsecured ceiling. On a five-year personal loan at 6.3% APR, you'd pay approximately £486 a month, repaying around £29,200 in total: about £4,200 of interest. It's clean, fast, and your home is never pledged. For a project of this size, that's often the right call even though it isn't the cheapest possible rate.

Now add that same £25,000 to a mortgage at 4.4% over 25 years. The monthly cost drops to roughly £138 - a third of the loan figure - which is why equity release feels so much more affordable month to month. The catch is the term: stretched over 25 years, the total interest is considerably higher than the loan's £4,200, even at the lower rate. The lesson isn't "one is always better." It's that a low rate over a long term can cost more in absolute pounds than a higher rate over a short one. Decide whether you're optimising for monthly affordability or lifetime cost - they pull in opposite directions.

Two habits protect you here. First, always ask for the total amount repayable, not just the monthly figure - it's the honest comparison. Second, borrow the project total plus a 10---15% contingency in one facility. London jobs routinely uncover party-wall costs, scaffold licences (£500---£1,500) or structural surprises; a second emergency loan mid-build is almost always dearer than borrowing correctly once.

Eligibility, credit and what lenders check

For an unsecured loan, lenders assess your credit score, income, existing debts and affordability - the best rates need a clean file with no recent CCJs or defaults. For a secured loan, they also value your property and check your equity and loan-to-value. Strong income and a tidy credit history unlock the advertised representative rates.

Eligibility for home improvement loans in London works the same as anywhere in the UK, but the larger sums involved make the checks bite harder. Unsecured approval turns on your credit profile. Lenders want a good score, a stable income, manageable existing commitments, and no recent county court judgments, defaults or bankruptcy. A soft eligibility check - offered by most banks and comparison sites - tells you your likely chances without marking your file, and it's worth running before any full application. Space applications out: several hard searches in quick succession can dent your score at the exact moment you're trying to borrow.

Secured lending adds a property dimension. The lender values your home, calculates your equity, and prices the loan against your combined loan-to-value across first and second charges. Lower LTV and clean credit get you toward that 6.39% floor; higher LTV or adverse credit push you up the range. Because the loan is regulated by the Financial Conduct Authority, you receive the same consumer protections as a standard mortgage - but the underlying risk is real: it's your home on the charge.

One quietly powerful factor sits within your control: the quality of your project documentation. A lender assessing a renovation loan is reassured by a clear, itemised, fixed-price quote from a single contractor far more than by a vague estimate or a stack of separate trade prices. Which leads directly to the next question.

Should you finance through your builder?

Some renovation firms offer their own finance, usually a personal loan brokered through a third party. It's convenient but often pricier, because the rate includes the builder's commission. Arrange your own loan through a broker or lender and compare - but do use a fixed-price design-and-build contract to strengthen whatever application you make.

Builder-arranged finance is genuinely convenient: one conversation, one signature. The cost of that convenience is usually a higher rate, because the finance is brokered through a third-party lender and the builder's commission is baked in. As a rule, treat any finance a contractor offers as one quote to beat, not a default - compare it against the open market before you sign.

The genuinely valuable thing a builder brings to your financing isn't a loan product - it's a clean contract. A design-and-build firm that handles design, planning and construction under one roof gives you a single fixed-price contract and one itemised budget. That's the document a lender wants: no gaps between an architect's fee and a separate builder's estimate, no ambiguity about scope, one accountable party. It makes a loan or remortgage application faster and cleaner to approve.

This is where the model matters. Architecture-only firms hand you a design and then pass you to a separate builder - leaving you to reconcile two sets of costs for your lender. Our approach at Better Homes is one team, one contract, one budget, from first sketch to final handover, backed by a 10-year workmanship guarantee and £10M insurance. We don't provide financial advice, but hundreds of London homeowners have used our fixed-price documentation to get their finance signed off without friction.

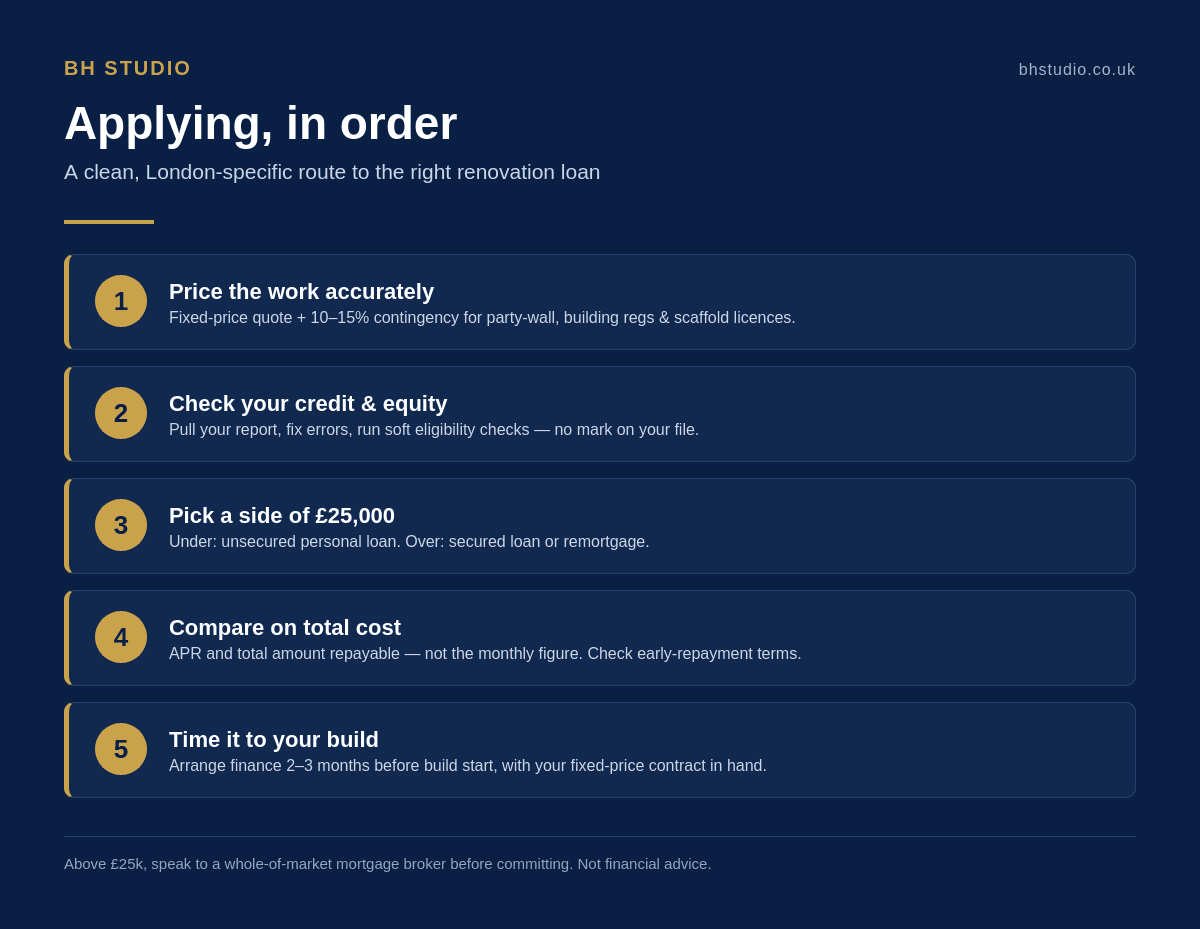

Applying: a clean, London-specific checklist

Price the work accurately first, including a 10---15% contingency. Check your credit file and run soft eligibility checks. Compare on APR and total repayable, not monthly cost. For sums over £25,000, speak to a mortgage broker about secured options. Then apply with a fixed-price contract in hand.

The sequence matters as much as the steps. Start with the real number: get a detailed, fixed-price quote for the whole project, then add 10---15% for the London-specific costs that ambush under-prepared budgets - party-wall awards (£1,000---£3,000 per neighbour), building regulations (£1,200---£2,500), scaffold licences, skip permits. Borrowing to a realistic total once is always cheaper than a second facility later.

With the number fixed, look at yourself the way a lender will. Pull your credit report, correct any errors, and run soft eligibility checks with two or three lenders to see your likely rate without marking your file. If the project sits under £25,000 and your credit is strong, an unsecured personal loan is probably your route - compare shortlisted deals on representative APR and total amount repayable, and check for early-repayment terms if you might clear it ahead of schedule.

If the project is above £25,000 - which, for a loft conversion or extension in London, it usually is - book time with a whole-of-market mortgage broker before committing to any single product. They can model a secured loan against a remortgage and a further advance using your actual mortgage terms, which is the only way to know which is genuinely cheapest for you. Time your finance to land 2---3 months before your build start, so funds are ready when your contract is signed and your first stage payment falls due.

Quick takeaways

1. The decisive number is £25,000 - the point most unsecured loans stop and most London space-adding projects begin.

2. Unsecured personal loans: fast, no property risk, £1,000---£25,000 (some to £35k---£50k), 5.9---7.4% representative for prime borrowers in mid-2026.

3. Secured loans: larger sums into six figures, 6.39---12% in June 2026, your home as collateral - and now used for a third of new second-charge agreements.

4. Compare on APR and total amount repayable, never the monthly figure alone - a long term hides a large lifetime cost.

5. Above £25,000, a broker-modelled remortgage or further advance usually beats any loan; below it, a personal loan's simplicity often wins.

6. A fixed-price design-and-build contract is the single best thing you can put in front of a lender.

7. Borrow the project total plus 10---15% contingency in one facility - London surprises are the rule, not the exception.

Getting the borrowing right before you build

Home improvement loans in London are simple products wrapped around a consequential decision. Get the type right - unsecured for smaller work, secured or equity release for the space-adding projects that define London renovation - and the finance quietly supports your build. Get it wrong, and you're either paying over the odds on an oversized personal loan or scrambling for an expensive top-up halfway through. The whole thing turns on two numbers you control before you ever approach a lender: an accurate project cost, and an honest read of your own credit and equity.

That's where the order of operations pays off. Price the work properly, add a real contingency, decide which side of the £25,000 line you're on, and compare on total cost, not monthly comfort. For anything above that line, a whole-of-market broker will save you more than their fee. And whichever route you choose, a single fixed-price contract from one accountable team is the document that turns a slow, uncertain application into a fast, clean approval.

At Better Homes, we design, plan and build loft conversions, extensions and full renovations across Central, East and North London - one team, one contract, one budget, backed by a 10-year workmanship guarantee and £10M insurance. We don't give financial advice, but the clear, itemised cost breakdown we provide is exactly what lenders want to see, and it's the starting point for every sensible borrowing decision. Book a free, no-obligation consultation and we'll give you the realistic project estimate your finance decision depends on.

We'd love to hear from you

Did you fund your London renovation with a loan, a remortgage, or a mix of both - and would you structure it the same way again? Share your experience in the comments or on social media. Your numbers could help another homeowner choose better. And if this guide clarified the £25,000 question for you, pass it to a friend weighing up how to pay for their project.

Frequently asked questions

What is the best way to pay for a home renovation in London?

It depends on the project size. Under £25,000, an unsecured personal loan is usually simplest - fast, with no risk to your home. Between £25,000 and £150,000, where most London extensions and loft conversions sit, remortgaging or a further advance is typically the cheapest per pound borrowed. Using savings avoids interest entirely, but keep an emergency buffer intact. Many London homeowners blend savings with borrowing.

How much can I borrow with a home improvement loan in the UK?

Unsecured personal loans for home improvements typically run £1,000---£25,000, with some lenders reaching £35,000 or £50,000 for strong applicants. Secured loans (second-charge mortgages) start where those stop and can reach £100,000 or more, depending on your property's value and the equity you hold. In London, where a rear dormer starts near £45,000, larger projects almost always need secured borrowing or equity release.

Is a secured or unsecured home improvement loan better?

Unsecured loans are faster, put nothing at risk, and suit projects under £25,000. Secured loans offer lower rates and much larger sums, but your home is used as collateral and the process takes weeks rather than days. For most London renovations, the project cost makes the decision: below £25,000 lean unsecured; above it, secured borrowing or a remortgage is usually both necessary and cheaper.

What APR should I expect on a home improvement loan in 2026?

In mid-2026, market-leading unsecured loans carry representative APRs of about 5.9---7.4% for prime borrowers, with maximums up to 29.9% depending on your credit profile. Secured loans run from roughly 6.39% at low loan-to-value to around 12% for higher LTV or adverse credit. The Bank of England base rate is 3.75%, held through Q2 2026, so pricing has been broadly stable.

How can I finance a loft conversion in London?

Because London loft conversions typically cost £45,000---£100,000+, they usually exceed unsecured loan limits. The common routes are a remortgage, a further advance from your existing lender, or a secured (second-charge) loan. A personal loan can cover a basic Velux conversion at the lower end, or top up a larger project mostly funded from savings or equity. Our complete loft conversion guide sets out the real costs by type.

Do I need to tell my mortgage lender about my renovation?

Yes. Most mortgage terms require you to notify your lender of structural alterations, and you'll need to update your buildings insurance to cover the work during construction and the higher rebuild value afterward. This applies whether you fund the work with a loan or by releasing equity. Failing to inform your insurer could invalidate your cover.

Should I take finance through my loft conversion or extension company?

You can, but compare it against the open market first. Builder-brokered finance is convenient but usually carries a higher rate, because it's arranged through a third-party lender and includes the builder's commission. What genuinely helps every application, wherever you source the money, is a clear fixed-price contract from a reputable design-and-build company - lenders approve well-documented projects faster.

References

1. Forbes Advisor UK - Compare Our Best Home Improvement Loans - representative APRs and lender loan limits, mid-2026.

2. MoneySuperMarket - Compare Home Improvement Loans - average market APRs and borrowing ranges, 2026.

3. Secured Loan Rates - Home Improvement Loans UK: Funding Your Renovation in 2026 - June 2026 secured loan pricing, base rate context and FLA second-charge data.

4. Money to the Masses - How to Get a Loan for Home Improvements (May 2026) - unsecured loan caps, application process and APR guidance.

5. GOV.UK / Bank of England - Bank Rate - official UK base rate, held at 3.75% through Q2 2026.

Last updated: July 2026. This guide is general information for London homeowners and does not constitute regulated financial advice or a personal recommendation. Always compare products on their full terms and consider independent guidance before borrowing.

Want Advice for Your Own Home?

We can help you translate this guidance into a realistic scope and execution plan for your property, whether you're considering a house extension, loft conversion or a full renovation.